7:36 AM

7:36 AM

febry

febry

PSP Investments' second Annual Public Meeting was held on October 28, 2010. You can consult the website's Annual Public Meetings section to download presentations and listen to audio recordings of the proceedings.

PSP Investments' second Annual Public Meeting was held on October 28, 2010. You can consult the website's Annual Public Meetings section to download presentations and listen to audio recordings of the proceedings.Let's first go over some sections of the speaking notes of Paul Cantor, Chair of the Board of Directors:

As I observed in the 2010 Annual Report, the first 10 years of PSP Investments were challenging times. According to the Wall Street Journal, the first decade of the 21st century turned out to be the worst ever for US stocks based on records going back to the 1830s. Total returns for the period 2000-2009 amounted to negative 0.5%. That compared with a high of 18% in the 1950s and was even lower than the negative 0.2% return for the 1930s Depression era.

In short, it proved to be an inopportune time to launch a new fund. Nevertheless, PSP Investments has grown into a robust, highly diversified fund that will soon rank among the largest pension investment managers in Canada and internationally. Assets under management now exceed $50 billion and the organization has more than 330 employees. PSP Investments has investments on every continent north of Antarctica.

Very true, the timing of this fund couldn't have been worse, but a decision was made to diversify away from non-marketable government bonds and over the long-run, this is the wise thing to do. As Mr. Cantor states further down:

The fundamental premise of the Board is that PSP Investments cannot achieve its desired objective for long-term returns of 4.3% — plus inflation — by investing in bonds. We can only achieve that by investing in other securities as well, such as equities. Of course, as events of the past two years underscored, markets are cyclical.

History has shown us that short-term volatility has always been part of equity investing. History has also shown us, however, that in the very long run markets have gone up more than they have gone down and that stocks have outperformed other asset classes over the long-term.

A note of caution here. Relying too much on history can be problematic given the structural nature of today's market and the unprecedented economic uncertainty that may loom for a prolonged period as developed nations struggle with the burden of debt. Moreover, as was mentioned a few days ago on the retirement disaster that lies ahead, even if you diversify away into stocks and alternative investments, investors will be lucky to achieve a real return of 2.1%.

Mr. Cantor goes on to state:

Thus it is important to not lose courage and sell when the markets decline; because chances are we would not be there in time to catch the wave when they rebound.

On that note, I am pleased to observe today that our patience has been rewarded: during fiscal year 2010, a substantial portion of unrealized losses from the downturn in the previous year was recovered. As at our March 31st year-end, PSP’s consolidated net assets had increased 37% to a new high of $46.3 billion and we earned a total portfolio return of 21.5%. In recent months, we passed the $50-billion mark in assets.

Those results underscore the solid long-term value of PSP Investment’s assets and also reflect initiatives taken to benefit from the market turnaround.

PSP enjoys an enviable liquidity advantage in that it does not have to pay out benefits for several more years. What that means is that unlike other pension funds, they weren't forced to sell stocks at the bottom to shore up liquidity. Deep pockets means you can keep buying the dips and sit tight waiting for markets to eventually turn around.

Mr. Cantor also spoke of reviewing PSP's Policy Portfolio:

Over the past few months we have undertaken a comprehensive review of the Policy Portfolio to ensure that it remains effective in delivering the expected returns. This review was enhanced by a significant strengthening of our ability to review the liability structure of our Funds and to link those with our asset allocation strategy.

The current Policy Portfolio has remained essentially constant since fiscal year 2006, when the last full review was performed. It reflects the diversification strategy initiated in fiscal year 2004 with the introduction of private asset classes — real estate in 2004, followed by private equity in fiscal year 2005 and infrastructure in 2006 — as well as the addition of the small-cap and emerging markets equity asset classes in fiscal year 2005.

The review takes into account the most recent expectations of long-term market conditions developed by PSP’s Economics and Market Strategy group. However, it is not only the market risks and volatility of returns that are being assessed.

The review also looked at another crucial consideration — the funding risk, that is the impact of the volatility of investment returns on the probability that a funding deficit will occur and on the stability of funding requirements.

Simply put, we want to ascertain that any funding deficit or changes in funding requirements as a result of investment returns would remain — under normal circumstances — within an acceptable range, while recognizing that we need to take on risks to achieve the real return objective.

Here too I will caution Mr. Cantor and the board of directors at PSP. Given that PSP is a fully funded plan, funding risks must be taken into account when constructing a Policy Portfolio. But the construction of a Policy Portfolio is tricky, especially nowadays.

My recent discussion with Leo de Bever highlighted some of the concerns that all pension funds are struggling with right now. Mr. de Bever isn't convinced that you can identify top quartile asset managers a priori and he feels that the shift into alternative investments will bring down the expected returns in illiquid asset classes as they become more "efficient".

Importantly, when reviewing your Policy Portfolio in this environment, you need to bear in mind what your peers are also doing. As silly as that sounds, it's crucial or else you risk overestimating the expected returns on an asset class. You also need to understand the long-term structural changes that are going to take place over the next decades. This is anyone's best guess, but a critical qualitative assessment is needed, and don't make the mistake of relying on quantitative analysis based on historical data.

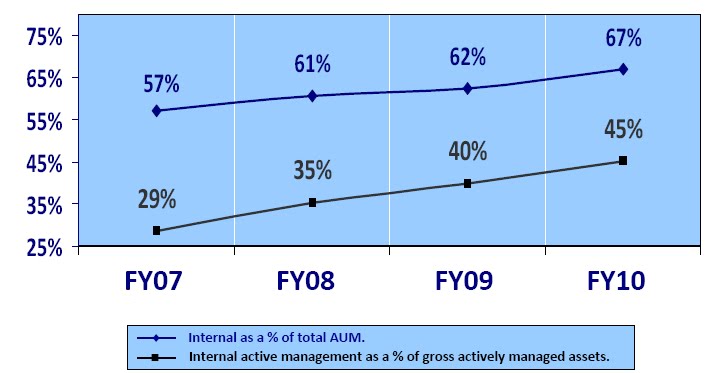

Gordon Fyfe, President & CEO, presented PSP's fiscal 2010 results. The entire presentation and the accompanying audio are worth going over and listening to carefully. Some of the key themes covered were PSP's diversification (see chart above) and the move to bring assets internally. In fact, as shown on the chart below from page 12, more assets are managed internally and a great proportion of active management is internal.

The savings of such a move are significant. According to Mr. Fyfe, external active management is 3.5 to 7 times more expensive and outsourcing all assets to fund managers would cost approximately $140 million more per year.

In terms of returns, it was interesting to note that the top five private investments accounted for a significant portion of value added in fiscal 2010:

Another interesting thing I caught on audio was that 2 deals - Telesat and China Network Systems accounted for the bulk of the gains in private equity. Mr. Fyfe said the PE team reviewed many deals but only chose a select few for direct investments.

Finally, there is a big push to go into emerging markets - both in public and private markets. PSP's performance in the first six months of fiscal 2011 is 5%, but that doesn't include the performance of private markets which are valued once a year at the end of the fiscal year.

All in all, I thought this was a good presentation. Would have liked to have seen a discussion on benchmarks and compensation, but they steered clear of those issues. Also, it was surprising that nobody bothered asking any questions during the Q & A and that once again this year, no media covered PSP's annual meeting (no excuses, the media had ample warning time to do so as the announcement was posted on PSP's site for a few weeks). Once again, PSP is flying under the radar, which suits Mr. Fyfe and his senior management team fine. They prefer delivering the results and staying out of the limelight.

***Feedback***

Here is some feedback from people who attended the meeting:

- The PSP fund was put in place in 2000 with the objective to reduce the government expenditures relating to public sector pensions. Gordon often refers indirectly to this objective by comparing the fund yield to the Chief Actuary's long term investment assumption of 4.3% plus inflation. By limiting his comparison to the period corresponding to the years since when he was appointed is good only to the extent that it assesses the performance of the fund since he joined. What the constituents need (and should want to know) is how is the fund performing since day 1 (2000). It happens that the cumulative yield minus inflation is over 4.3% since 2004 but under 4.3% since day 1 (2000).

- I agree with you that any information regarding performance benchmarks and compensation practices was noticeably absent from the PSP Investments presentation. During the morning session, I raised a concern with CEO Gordon Fyfe regarding the increasing proportion of the PSP Investments portfolio dedicated to foreign asset classes and what corresponding risk management practices had been put in place along with

this development.